To determine the true cost of a product, you need to calculate direct materials, direct labor, overheads, waste, subcontracting, energy, and depreciation costs together. A common mistake in footwear, textile, leather, furniture, metal, and packaging manufacturing is limiting the cost to the material amount listed in the bill of materials.

Before calculating the estimated cost, it is necessary to conduct the required engineering studies to determine the quantities that will form the basis of the estimated cost. This includes conducting land and soil surveys, preparing projects (implementation projects for building works, implementation projects for parts of other works where it is possible, and final projects for parts where it is not), preparing bill of quantities and price lists, and determining the prices and market rates that will form the basis of the estimated cost calculation.

To determine the true cost of a product, you need to calculate direct materials, direct labor, overheads, waste, subcontracting, energy, and depreciation costs together. A common mistake in footwear, textile, leather, furniture, metal, and packaging manufacturing is limiting the cost to the material amount listed in the bill of materials.

Pricing is the process of determining the price a product or service costs at which a customer is willing to buy and a business is willing to sell. Choosing the right price can help increase revenue and profits, satisfy market demands, and build customer loyalty. The price a consumer is willing to pay is not tied to a company's costs. Buyers are more interested in the value they receive from a product or service.

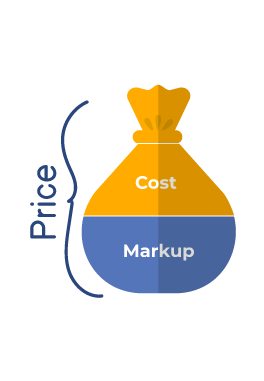

The price of a product consists of two components: cost price and markup. Cost price is the cost of acquiring or producing the product itself. Cost price, in turn, is made up of the following costs: Direct costs – production expenses: raw materials, employee wages; for retail: product acquisition costs. Indirect costs – those not directly related to the production or procurement of goods.

Internal factors are those that a company can control. Cost price. This is all the company's expenses for the production and sale of products or services. The higher the costs, the lower the profit and profitability of the enterprise. Price segment. These are groups into which products with similar properties and prices can be divided. Life cycle stage. Depending on the stage of a product's development, its price will vary. Product quality. Production characteristics.

Customer acquisition cost, or CAC, literally translates as "the cost of attracting a customer." CAC measures how much each new customer costs a company. It's one of the most basic and common metrics in marketing. The principle for calculating CAC is always the same: marketing expenses are divided by the number of customers acquired. Costing of services is an assessment of the costs associated with performing work on a client's order. It is used to determine planned or actual costs. Costing of services is necessary to determine: actual cost; the total cost, taking into account standards; profitability; labor intensity; the productivity of individual teams; cost reduction methods; and labor and material reserves.

Cost is the amount of money spent by a seller or manufacturer to create a product or purchase it from a supplier. Cost is the sum of all expenses: production, logistics, warehouse rent, and staff salaries. Cost also includes other components: time, effort, and the value of the product. From these elements, the seller calculates a markup on the cost price.

Interest on loans used to finance investments must be added to the investment cost to be amortized along with the fixed asset if it pertains to the establishment period; interest pertaining to the operating period must be expensed directly in the years to which it relates or amortized by being included in the cost. Exchange rate differences arising from the valuation of installments related to fixed asset imports from abroad using foreign currency loans, either during or after the import, must be added to the cost of the asset up to the end of the period in which the fixed asset was acquired.

To calculate SSY or TSY using this method, the cost of the equipment at the time of delivery must be known. In this method, items included in direct expenditures are calculated as a percentage of the equipment cost. Other items in capital investment are calculated as a percentage of the direct cost. This method is used to calculate the investment cost of a new, similar facility with a different capacity by utilizing the cost of a previously constructed facility.

Turnover Ratio = Gross annual sales / Fixed capital investment. Turnover Ratio = 1 / Capital ratio.

By combining these elements, businesses can achieve realistic pricing and cost control, gain a competitive advantage, and realize sustainable profitability.